Common questions others ask

One of the most common conversations we have at 316 Health Insurance is helping our clients who are considering retirement develop a winning exit strategy for their health insurance needs. We explore and explain their options for COBRA, how to purchase insurance through the individual Marketplace, what other coverage options are available to them, how their pre-existing conditions are handled, whether or not they can leverage subsidies or Advanced Premium Tax Credits (APTCs) to help them pay for their insurance, and how they can successfully bridge the gap until they become eligible for Medicare.

Many of our clients come to us from their financial advisor or their estate planning attorney, because figuring out their health insurance is an integral part of their retirement planning. We work hand-in-hand with their current trusted advisors to help them put together all the pieces for their retirement.

While the topic may seem daunting to them at first, typically after our initial consultation, our clients leave with confidence as they face their retirement health insurance decisions. Often, our clients come to us initially saying things like, “I am only working for the insurance,” or “If we can figure out how to affordable cover our health insurance, we would retire sooner-rather-than-later!” More often than not, they find that solving their health insurance problem in retirement is not nearly as scary as they feared; and that they can retire when they are ready to, rather than feeling trapped by their group health insurance.

You have worked hard to save and prepare for retirement. Don’t let the fear of figuring out how your health insurance will work in retirement keep you from enjoying your golden years! You’ll be surprised at how simple and affordable the transitional process can be without sacrificing your peace of mind for quality coverage.

When our clients come to us, there isn’t much they need to bring with them besides their health insurance problems. However, it is also helpful if they can bring with them a basic knowledge of their health history, what medications they are taking (if any), and a list of the providers they like to see. Knowing the basic details of their current coverage, as well as their options through work/COBRA (including costs) helps our advisor team lay out every option available to them so our clients can make informed, confident decisions.

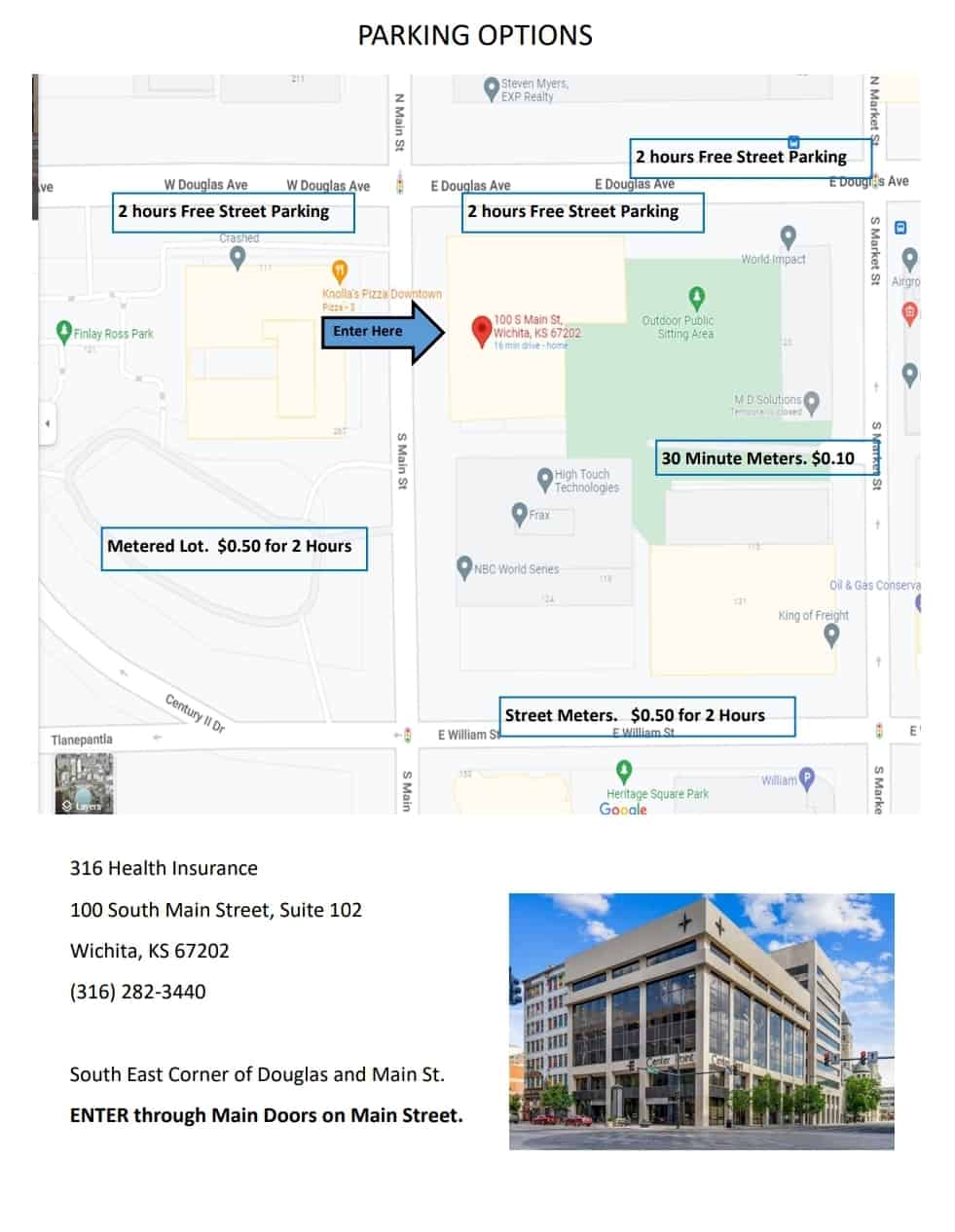

We are located on the main floor of the Center Point Building on the SE corner of Douglas and Main St in downtown Wichita. The physical address is 100 S Main St, Suite 102. You can see our 316 Health Insurance Sign on Douglas, but the entrance to the building is around the corner on Main St. Once inside the building, walk towards the elevators to the second door on the left. You will see our sign and our office! Come on in, and you will be greeted by our client care coordinator!

Parking for 316 Health Insurance is very simple. Click HERE to download a PDF map or HERE to download a picture map to parking around the building. Typically, there is free parking up and down Douglas. For those who prefer a more sure place to park, there is always room in the metered parking lot across the street from the building entrance to the southwest. The meters take quarters only. If you chose to park there, please grab some quarters from our reception desk to cover your parking. If you don’t have any quarters with you when you park, it is ok! Just let us know when you come inside, and we will be happy to run out to make sure your meter is taken care of.

{kind=link}

We ALWAYS prefer seeing our clients in person. We feel that the flow of communication is always much easier face-to-face. However, we do have the ability to hold our consultations virtually via zoom for our out-of-town clients, or for our clients who just can’t quite get to the office.

The Affordable Care Act (also known as the ACA, PPACA, “Marketplace Insurance”, or “Obama-care”) is a comprehensive health insurance law passed in 2010 that completely shifted how health insurance companies deal with pre-existing conditions. It also provided consumers with access to federal money through Advanced Premium Tax Credits (APTCs) or “subsidies” to help them curb the high-cost of health care. In addition, the ACA set Minimum Essential Coverage (MEC) standards for all qualifying health plans. These MEC standards include things like preventative care, mental health benefits, prescription coverage, emergency services, and more.

Most Americans become eligible to receive their Medicare benefits on the first day of the month in which they turn 65. As that date approaches, many of our clients get overwhelmed with the amount of mail, phone calls, tv ads, and email trying to pressure them into making a Medicare decision. They feel intimidated, confused, and unsure of what to do. At 316 Health Insurance, we are committed to providing our Medicare-eligible clients a better way. We do this by sitting down for a Medicare Strategy meeting, where we unpack for them what Medicare is, how it works, and what decisions they need to make as it pertains to Medicare Supplements, Part C – Medicare Advantage, and Part D – Prescription Coverage. We do this in a safe, non-salesy environment so that our clients can move forward with confidence.

This is a very common question for our agency; one that we have helped many of our clients answer. We always welcome our clients about to turn 26 to what we call the “final stage of adulting”, which happens when you have to buy your own health insurance for the first time! We have a proven system that helps these clients understand what health insurance is, how it works, and what to expect as they move forward. We then educate and empower them to decide with confidence the best choice for them based upon their budget. We explain things like co-pays, deductibles, direct primary care medicine, subsidies, co-insurance, max-out-of-pocket, and sharing plans. It always brings us great personal satisfaction as an agency when we see our first-time health insurance buyers leave with a smile on their face and relief in their eyes!

Christian Sharing Plans and Medical Cost Sharing Programs are alternative ways that people can mitigate their health insurance risk. While these programs are NOT insurance, they use a membership-based risk pool to help their members share health needs as they arise. In addition, many Chrisitian Sharing Plans are also eligible options under the ACA as it pertains to the individual mandate. While Sharing Programs can be an attractive alternative to health insurance, we educate our clients to understand that they are NOT health insurance, nor are they regulated by the State Insurance Department. While these programs do not deny membership based on pre-existing conditions, many of them place exclusions and/or waiting periods on them. In addition, they have standards for accountable, healthy living choices in order for them to share health needs.

Insurance terminology can be incredibly confusing, especially since health insurance doesn’t quite work the same as home/auto insurance. In a nutshell, here’s what these terms mean:

- Copay: A copay is a set amount of money an insured spends in order to receive a health service. These copays are not subject to a deductible first. Examples of copay items are doctor visits, prescription costs, and specialist visits, where an insured will pay a set fee at the time of service.

- Deductible: A deductible is the amount of money that must be spent by an insured before gaining access to health benefits on their policy. Typically, hospital charges, outpatient surgery, ER visits, and diagnostic testing are subject to a deductible first before benefits are paid. The higher the deductible is on a health insurance policy, the lower the monthly premium is.

- Co-insurance: After a person meets their deductible on their health insurance policy, typically they enter into the “co-insurance” phase of their coverage. The co-insurance is the “split” (ie, 80/20, 70/30, 60/40) where the insurance company pays the first number as a percentage of every dollar spent, and the insured pays the second number as a percentage of every dollar spent. So a 70/30 coinsurance means that the insurance company will pay 70 cents of every dollar, while the insured will pay 30 cents.

- Maximum Out of Pocket: The out-of-pocket max is the MOST an insured will have to pay for all their covered in-network health services within a given health year. In other words, when an insured hits a certain number when adding up their copays, deductible, and co-insurance, the health plan will then pay 100% of eligible, in-network costs for the remainder of the policy year.

Most health insurance policies not only have an “individual” deductible and/or out-of-pocket maximum, they also have a “family” deductible and/or out-of-pocket maximum.

We work hard to make sure our clients have access to the doctors and hospitals of their choosing. Different insurance carriers work with different providers. We take the time to evaluate the various networks to find the best match for every client.

The Affordable Care Act provides “subsidies” or Advanced Premium Tax Credits (APTCs) to help people that buy health insurance on their own. In order to use these subsidies, a person cannot have access to “affordable” health insurance through other means, including an employer-based health plan. For 2022, a group health plan through an employer is considered affordable if individual coverage (for just the employee – not including their family members) costs less than 9.61% of their 2022 household income. In addition, if a person qualifies for Medicare, VA benefits, or state Medicaid, they are unable to leverage federal subsidies to purchase health insurance through the Affordable Care Act. People who wrongly take federal subsidies to purchase health insurance through the ACA open themselves up to having to pay those subsidies back on their tax return, plus penalties and interest. It is imperative that people using subsidies through the ACA do so the right way to stay out of potential tax trouble when they do that year’s taxes. At 316 Health Insurance, we understand how this system works, and help our clients mitigate the risk of doing it incorrectly.

Yes. We sit down with our Medicare clients in a safe, non-salesy environment, then explain how Medicare works. We take the time to discuss the history of Medicare from its inception in 1965, through its evolution into the system we have today. We talk about the four parts of Medicare: A, B, C, and D. We explain the standardized Medicare Supplements (or Medigap Policies) that are available, and how they work. Then we unpack Medicare Advantage, discussing the pros and cons of each option. We love to have these “Medicare Strategy Conversations” months before our clients actually become eligible for Medicare so that they are educated and empowered to make decisions with confidence as they enter their Medicare eligibility.

When the Affordable Care Act was enacted, it carried with it an individual mandate, requiring Americans to be enrolled in a qualified health plan, or be a part of an ACA-eligible Sharing Program. Those who did not were subject to a tax-penalty based on their Modified Adjusted Gross Income and the number of people in their household who did not carry qualified coverage. In 2019, the penalty for not carrying meeting these standards was set to $0, but the mandate that requires Americans to have a Qualified Health Plan or be enrolled in an ACA-eligible Sharing Program remains. In short, the individual mandate of the ACA is still in effect, but the penalty for not meeting those standards has been done away with.

Health insurance purchased through the Federally Facilitated Marketplace (FFM) are not subject to pre-existing condition limitations. In other words, those with health concerns can rest assured that their conditions will be covered from “day 1” of their coverage in an ACA plan.

Part of what we do when we advise our clients is to help them navigate the plans, prices, networks, prescriptions, and coverage options through the ACA. In 2022, in Sedgwick County alone, there are 64 different plans available for people to purchase across 5 different companies. We have systems in place to help our clients discover the plans that give them the experience they want at the price they can afford.

As health insurance premiums continue to rise, most businesses have stopped contributing towards the cost for an employee’s family members to be covered on the group plan; meaning that an employee will pay full price to add his/her family members to the insurance plan offered at work. Many times, a family can save premium costs and increase their coverage by shopping for health care through the individual market. Our team at 316 Health Insurance can help you look at all available options – including ACA plans, private plans not offered on the exchange, sharing programs, Direct Primary Medicine – to help you find the answer. Often the solution involves blending together a variety of options to give you the experience you want at the price you want to pay.

LESS CONFUSION, MORE SUPPORT

Why 316 Health Insurance?

- We don’t use high pressure sales tactics.

- We listen to your needs and are compassionate about your situation.

- We do what is best for YOU, regardless of commission.

- We work to solve your problems, not just sell you products.

We are here to help! No pressure-filled, predatory or confusing tactics – just clear, supportive help from a trusted local insurance advisor.

Kind Words From Clients

Next Steps

Working with 316 Health Insurance.

It is as Easy as 1, 2, 3...

STEP ONE

Schedule a consultation

We have 3 convenient ways for you to connect with us:

STEP TWO

Meet with an advisor

Prior to your meeting, we will send you detailed information on what to expect, what to bring, and where we are located.

STEP THREE

implement Your Strategy

We will walk with you every step of the way once you have decided on your path moving forward, from application/enrollment, to payment options, to claims handling, to “red-carpet” long-term client care.